Brief Summary

This video provides a comprehensive introduction to basic accounting concepts, ideal for those without a commerce background. It covers the definition of accounting, the accounting process, the five elements of financial statements (assets, expenses, liabilities, equity, and revenue), the double-entry system, and debit/credit balances.

- Accounting involves recording, classifying, and summarising financial data into a meaningful format for users.

- The accounting process starts with source documents and culminates in financial statements.

- The double-entry system records two aspects of every transaction: debit and credit.

Intro

The video is an introduction to the basic concepts of accounting, tailored for science students or those without a commerce background. It promises a simple and straightforward explanation of accounting principles, processes, debit, and credit. The presenter encourages viewers to watch until the end for a practical and logical understanding of accounting.

What is Accountancy?

Accounting involves recording, classifying, and summarising financial data into a meaningful format. This format is essential for users of financial information, such as management, shareholders, the government, and creditors, to make informed decisions. The meaningful formats are the balance sheet, which shows the financial position of the company, and the profit and loss account, which shows the financial performance and profitability of the company.

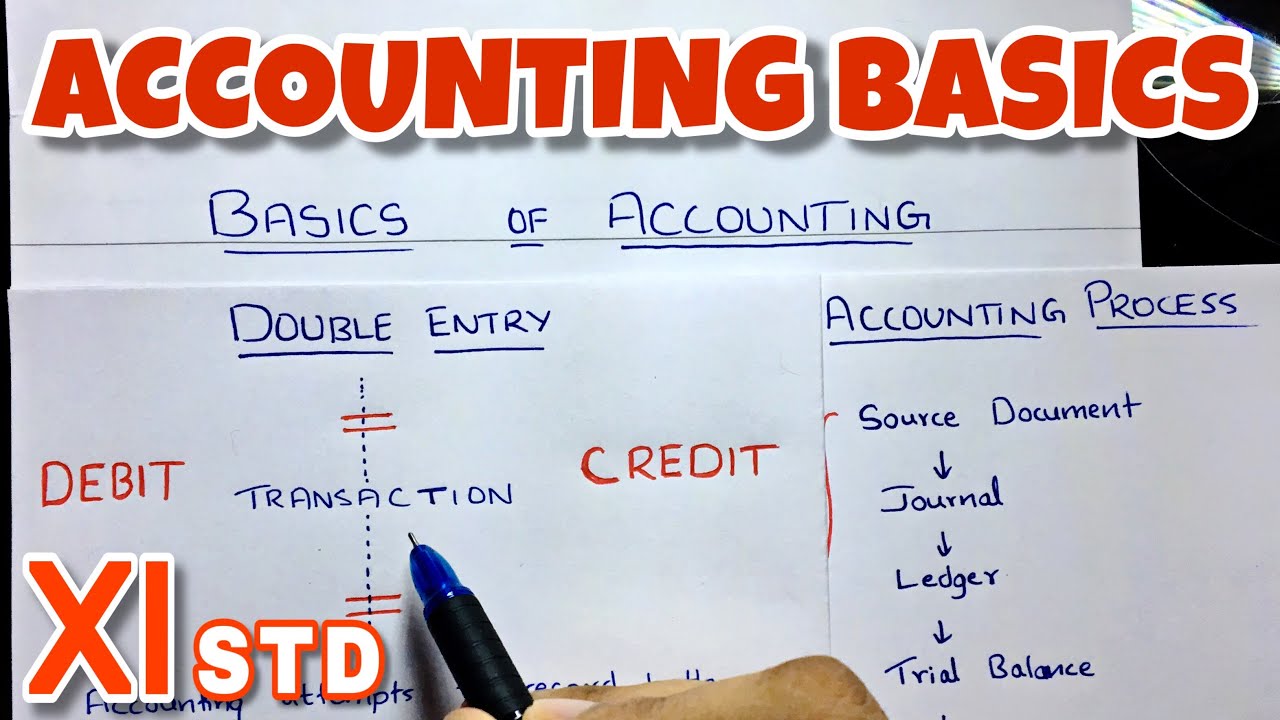

Accounting Process

The accounting process begins with a source document, which serves as evidence for a transaction. Based on this document, a journal entry is made in the journal book. Ledger accounts are then created, and their balances are summarised in a trial balance. Finally, financial statements, including the balance sheet and profit and loss account, are prepared. The steps from the source document to the trial balance are referred to as bookkeeping, a task typically performed by an accountant.

5 Elements of Financial Statements

There are five core elements in accounting: assets, expenses, liabilities, equity (or capital), and revenue (or income). These elements are represented on financial statements, with expenses and revenue appearing on the profit and loss statement, and assets, liabilities, and equity appearing on the balance sheet. The entire accounting system is based around these five elements.

Asset?

An asset is a resource controlled by an entity as a result of past events, from which future economic benefits are expected to flow. Control can be through ownership or a lease agreement. Future economic benefits refer to the potential of the asset to generate revenue or contribute to the company's operations. The definition has shifted from mere ownership to control and expected future benefits.

Expense?

An expense is the cost of operations a company incurs to generate revenue, without any further expected benefit. The key difference between an asset and an expense is that with an expense, the benefit has already been realised. Examples include rent and salaries, where the benefit is consumed immediately upon payment.

Liability?

A liability is a present obligation of an entity to transfer an economic resource as a result of a past event. This means the company has a duty to pay or do something, such as paying a supplier for goods purchased on credit. Liabilities represent claims of outsiders on the total assets of the company.

Equity or Capital?

Capital is the money invested by the owners of a business. The term "equity" is often used for companies where capital is divided into shares. Technically, equity is the residual interest in the total assets of the entity after deducting all its liabilities. It represents the owners' claim on the company's assets after all liabilities have been settled.

Revenue?

Revenue is the gross inflow of cash, receivables, or other consideration arising from the ordinary activities of a business. This includes sales of goods, rendering of services, interest received, and rent received. Essentially, it's the income a business generates.

Practical Example

A practical example illustrates the concepts of assets, liabilities, and equity using a sole proprietorship. Starting with an initial capital investment, the example shows how purchasing machinery and taking out a bank loan affect the balance sheet. The example clarifies how liabilities create an obligation to pay back, and how equity represents the owner's claim on the company's assets after deducting liabilities.

What is Double Entry System?

The double-entry system is an accounting method where every transaction is recorded with two aspects or effects: a debit and a credit. This system ensures that the accounting equation (assets = liabilities + equity) remains balanced. Every transaction has at least one debit and one credit, and the total value of debits must equal the total value of credits.

Debit and Credit Balances

Assets and expenses always have debit balances, while liabilities, equity, and revenue always have credit balances. To increase an asset or expense, you debit the account. To increase a liability, equity, or revenue, you credit the account. This understanding is crucial for passing journal entries and doing ledger postings. The presenter dispels the misconception that debit always means plus and credit always means minus, clarifying that the effect depends on the type of element.